Numbers mean nothing until they are acted upon.

In the finance world, deciding whether to let a number sway a decision is the role of financial managers. Frequently, the numbers are sourced from external auditors. As auditors are increasingly using AI tools, the question is, do their clients actually trust the output? Emily Griffith, Professor of Accounting at the Wisconsin School of Business, alongside Cassandra Estep and Nikki MacKenzie, researched how financial executives respond to financial reports and auditor oversight differently based on AI use.

“Empirical evidence shows that advanced technologies such as AI can improve financial reporting, but whether it will do so is unclear.”

Griffith’s work examines whether there is enough trust in AI data for the financial world to realize AI’s benefits.

Why use AI in auditing to begin with?

Some studies have found that AI auditing is more accurate and can take on some cumbersome tasks needed for financial auditing such as inventory. Part of the cause is that AI can perform functions too complex for humans to handle. With its massive data processing capabilities, machine learning can incorporate information not currently in a company’s estimation model. For example, it can process online reviews and customer feedback to assess whether a warranty covers the most common issues. Because AI is not a traditional employee, it is not motivated to provide optimistic reports, which can make its assessment a more reliable reflection of the current state. Benefits of AI will only accrue to the degree that financial managers take action based on AI-produced data.

The Experiment

115 financial executives, 62% of whom held CEO, CFO, or controller titles, were told to assess a patent valuation for a fictitious company. Valuation for a patent is not a straightforward accounting calculation, but rather an assessment of a variety of variables including the market, economic impacts, legal factors, and technology, making this an ideal example of a highly complex audit case. Provided with background data on the patent and an estimate of the value of the patent from an auditor, they were tasked with making a decision regarding the fair value of the patent.

To capture initial reactions, managers used a scale from 0 to 10 to rate the reasonableness of the audit results. The degree to which they acted on the auditors’ data was measured by how much they moved the initial patent valuation towards the auditors’ recommended valuation.

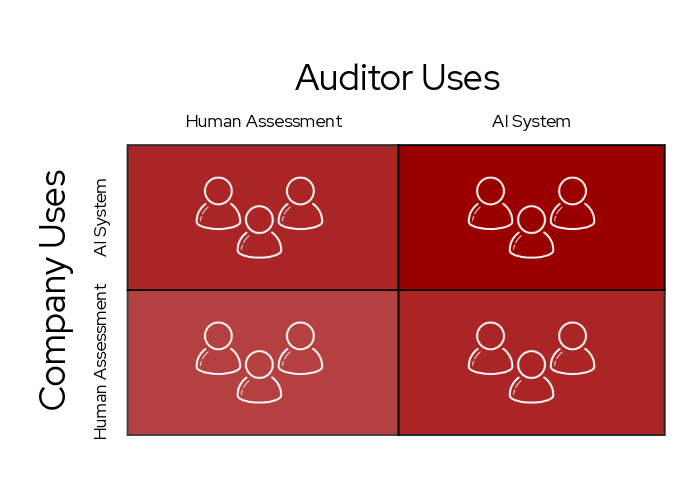

They were divided into four groups based on two dimensions. First, they were told the company used human valuation specialists or an AI system for internal financial reporting. Second, they were told that the audit firm used either a human auditor or a proprietary AI system to produce the estimate.

This produced measures of perceived reasonableness and financial impacts of trust in AI versus human audit sources.

The Results

The results provide two critical insights into the perception of AI versus human data.

First, how managers reacted to the AI-provided information has more to do with their own company’s AI usage than the audit source. When rating the reasonableness of the auditor’s data, the companies with only human processes rated the AI system’s valuation nearly equal to the human auditor’s. Companies already working with AI internally rated auditors’ AI outputs as far more reasonable.

Second, managers are not averse to AI-sourced data. In fact, some trust it even more than data from humans. How much they acted on the numbers revealed how much they trusted the source. This trust has high stakes. Among managers at companies using AI, the amount accepted from an AI system was nearly 20% closer to the auditor’s recommendation than the human-sourced audit. If this were a real patent, the gap would result in a $1,045,391 difference for the patent’s value. When managers’ companies use AI, they find the AI audit evidence to be more reasonable than an audit conducted by a human.

“This study illustrates the benefits of considering a decision context from multiple points of view. The survey reveals managers’ perceptions of their companies’ AI use, which inform our theoretical understanding of managers’ decisions in the experiment.”

What this means

Financial managers trust AI. Clients at less AI-savvy companies still trust AI outputs from their auditors almost as much as a person’s. AI-using companies trust it even more. The managers realizing the greatest gains from AI-sourced data are at companies that are already using AI. Auditors who use AI are producing data that managers are ready to act on.

Actions based on AI data can have considerable impacts on the larger organization. Patent valuation, which the study explored, is a clear example: how managers react to AI data can create wider financial implications. These valuations shape a company’s financial health and investor perceptions, particularly in today’s landscape now that companies’ assets are increasingly concentrated in technology and IP rather than physical capital.

This also signals to public accounting firms that adopting AI won’t damage how reasonable clients perceive their audit work, reducing the risk of implementing AI processes. For a client that is using AI internally, the bigger risk might actually be not using AI.

Quotes and findings are from “How do financial executives respond to the use of artificial intelligence in financial reporting and auditing?”, Review of Accounting Studies, (2024)

Read the full paper here.