In the U.S., employers must carry workers’ compensation insurance. These workers’ compensation insurance programs provide medical benefits and a portion of lost income to workers who are injured or become ill at work. But unlike other insurance markets, some states don’t leave this entirely to private companies — they have public options that compete directly with private insurers (and not just for the residual, or worst, risks). That unique setup raises a practical question: what happens to competition, performance, prices, and market stability when the government becomes an active player in an insurance market?

This is exactly what I set out to answer in my new study on workers’ compensation insurance markets, which is the first to empirically assess the effects of forming a public option – not to coordinate with the private market but to compete statewide for all risks – on U.S. insurance markets.

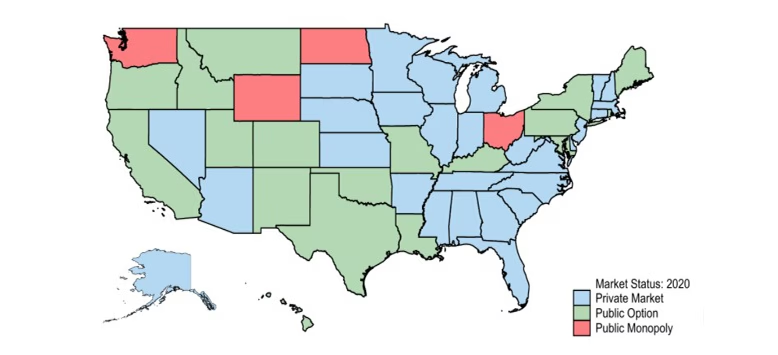

Workers’ Compensation Insurance Markets

As shown in the map above (for 2020, the last year of my data), the structure of workers’ compensation markets varies from state to state. In some states (in blue), workers’ compensation insurance is provided exclusively through the private market. In other states (in red), the government is the only seller. Yet, in 18 states (in green), the government competes with the private market via a public option.

In some states, public options have existed in workers’ compensation for over 100 years. Over the last 30 or so years, however, several states have formed new public options. I focus on six states that did so in the 1990s – Texas, Louisiana, Maine, Kentucky, Missouri, and Hawaii – to understand what forming a new public option might mean for the market.

Inside the Findings

My paper, which served as my showcase paper on the academic job market and is the first chapter of my dissertation, includes several key findings:

- Public options quickly gain market share. In states that introduced a public option, it quickly became a major player rather than a small, niche carrier. After more than 20 years in existence, in 2020, both a strong year for workers’ compensation insurance profitability nationally and the last year of my data, the public options I study still have more than 30% market share on average.

- Market concentration rises. Rather than making markets more competitive, the entry of public options tended to increase overall concentration. This suggests more and more employers were buying their insurance from fewer and fewer insurers.

- Underwriting looks better, but not because of the public option. Market-wide loss ratios improved after public options appeared, but much of this change was driven by broader policy changes (like cuts to legislated benefit levels) rather than public option entry.

- Public options often charge slightly higher prices. Yet their presence may help carve the market into segments and reduce private carrier volatility in loss experience.

Why This Matters

For employers and policymakers, these findings spotlight a subtle truth: government involvement doesn’t automatically mean more competition or lower costs. Rather, when the government becomes an active insurance competitor, it reshapes competition, pricing dynamics, and even how private firms manage risk. That doesn’t mean public options are necessarily bad; in some states, they provide private carriers with stability.

These empirical findings are the first on the impact of a statewide public option – competing for all risks, not only in coordination with the private market and not just as a backstop or insurer of last resort – in U.S. insurance markets. Public options in this setting are relevant right now, as well: in 2025, Missouri privatized its public option after 30 years in operation. Given that workers’ compensation benefits provide health and disability coverage to injured workers, the findings may also speak to other policy areas where public options have been hotly debated.

Tyler Q. Welch is graduating from the University of Wisconsin with a PhD this spring and will be joining Temple University’s Fox School of Business as a tenure-track Assistant Professor in the Department of Risk, Actuarial Science, Healthcare Management, and Legal Studies. To learn more about Tyler’s research, visit www.tqwelch.com.

Categories: