Key Observations: The two tax proposals we’ve analyzed (i.e., the reduction of the U.S. corporate tax rate to 20% and new limits on the deductibility of interest expense) have a net positive benefit on cash flow for highly levered transactions in many scenarios. However, in a downside scenario where revenues are declining, there is a significant negative impact on cash flow. We believe this may increase borrowing costs for highly levered transactions, especially in environments where downside risks are material.

Executive Summary

On November 2, the U.S. House Ways and Means Committee released the Republican tax reform bill, known as the Tax Cuts and Jobs Act. Although it is still subject to revision, two corporate tax provisions caught our attention at the Nicholas Center. First, the most significant revision on the corporate tax side is a reduction in the U.S. corporate tax rate. Second, a more overlooked revision would limit the deductibility of interest payments in certain instances.

Our biggest question was whether these tax proposals would positively or negatively impact levered transactions (e.g., levered buyouts or other highly levered transactions) and the private equity industry in general. Our analysis suggests that the positive impact of the reduction in the corporate tax rate would exceed the negative impact of the limitation of interest payment deductibility in many scenarios. Our viewpoint is corroborated by the share price performance of the publicly traded private equity firms (i.e., KKR, Carlyle, Blackstone and Ares Capital), which were up slightly or flat on the news. In addition, the Ares CFO stated on their earnings call on November 3 that “I think we should expect that it’s a net positive for the business.”

However, we believe there is a significant negative impact on cash flows in a downside scenario. Although this may be overlooked by equity markets today, we expect that lenders and credit markets will internalize this negative impact over time and potentially raise borrowing costs for highly levered transactions in environments where downside risks are material.

Proposed Changes to §3001 and §3301 of the Internal Revenue Code of 1986

The two provisions at issue are as follows:

- §3001 – the new tax proposal revises the U.S. corporate tax rate to a flat 20-percent rate beginning in 2018. Currently, U.S. taxable income above $10 million is taxed at a 35-percent rate.

- §3301 – the new tax proposal disallows a deduction for net interest expense in excess of 30 percent of a company’s adjusted taxable income. Adjusted taxable income excludes interest expense, interest income, net operating losses, depreciation, amortization and depletion. Any disallowance would be carried forward to the succeeding five taxable years. We also note that §3203 exempts companies with less than $25 million in sales from these interest limitation rules.

An Example to Illustrate the Impact of the Proposed Changes

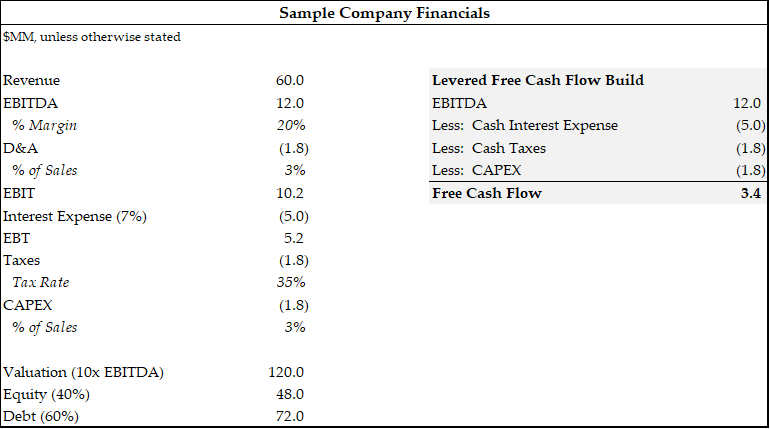

To understand the impacts of these proposed changes, we start with a set of assumptions about a hypothetical levered transaction. In the example below, a U.S.-based company with U.S. assets is purchased for $120 million, financed 40% with equity and 60% with debt. Based on the financial characteristics assumed below, this company would generate $3.4 million per year in levered free cash flow.

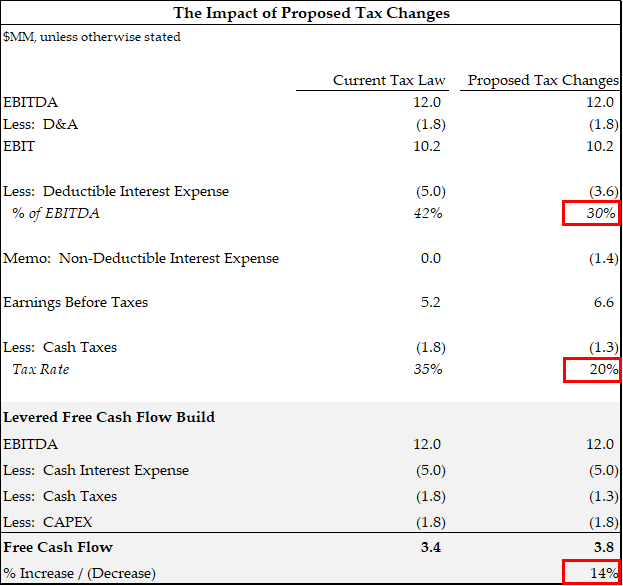

Under the proposed changes, the corporate tax rate is reduced from 35% to 20% and the company is not allowed to utilize the tax shield on any interest expense in excess of 30% of adjusted taxable income. We use EBITDA as a proxy for this given the definition of taxable income excludes depreciation, amortization, interest income and interest expense. We model these changes as follows:

As you can see, in this example, the annual free cash flow of this hypothetical levered transaction increased by 14% as a result of the proposed changes. The positive impact from the reduction in the corporate tax rate exceeded the negative impact of the loss in interest deductibility.

But When Is the Overall Impact Negative?

Next, we wanted to identify the scenarios in which the negative impact from the loss in interest deductibility would outweigh the positive impact of the reduction in the corporate tax rate. We found 2 such scenarios: (a) in a downside scenario and (b) in a rising interest rate environment.

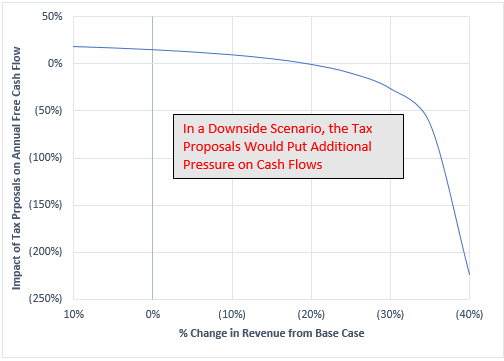

- Downside Scenario

We define a downside scenario as a percentage decrease in revenue. As you can see in the chart below, if revenue declines by more than 20%, the impact of the tax proposals on free cash flow is negative. In more extreme cases (e.g., a 40% revenue decline), the decrease in cash flow is 223% (i.e., from +$234K free cash flow under the current tax law to -$288K in the new proposal). We believe this is a significant downside risk that may increase borrowing costs for highly levered transactions because of the increased risk of bankruptcy.

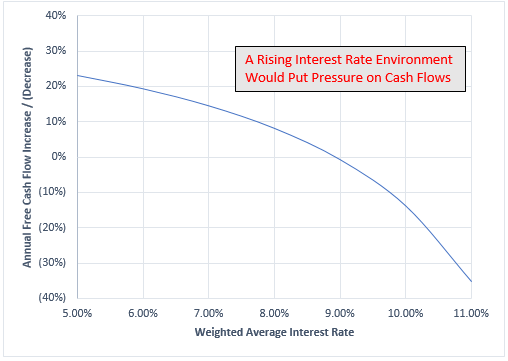

2. Rising Interest Rate Environment

If interest rates rise significantly, there is an overall negative impact on free cash flow.

Conclusion

The Republican Tax Bill has many proposals that need to be debated before becoming law, including the interest deductibility limits and the reduction in corporate tax rates. Overall, if these proposals are adopted, they appear to benefit firms that engage in levered transactions (e.g., private equity) in many scenarios. Of course, these transactions are better off if the interest deductibility limits are eliminated, but the overall reduction in the corporate tax rate exceeds this cost. However, we have identified a number of scenarios, the most important being the downside scenario, in which there is an overall negative impact on highly levered transactions.

Categories: